The AI Revolution No One’s Talking About

How Artificial Insemination reshaped the American beef supply

This is, on one level, a story about semen. On another level, it is a story about industrial organization. A technology that helped dairies solve one problem, replacement heifers, also gave them a new way into the beef business. The important question is not simply whether this adds much more beef in aggregate. It is whether reproductive technology has changed who gets to compete for value inside the cattle industry.

I think it has. This essay is my attempt to explain why.

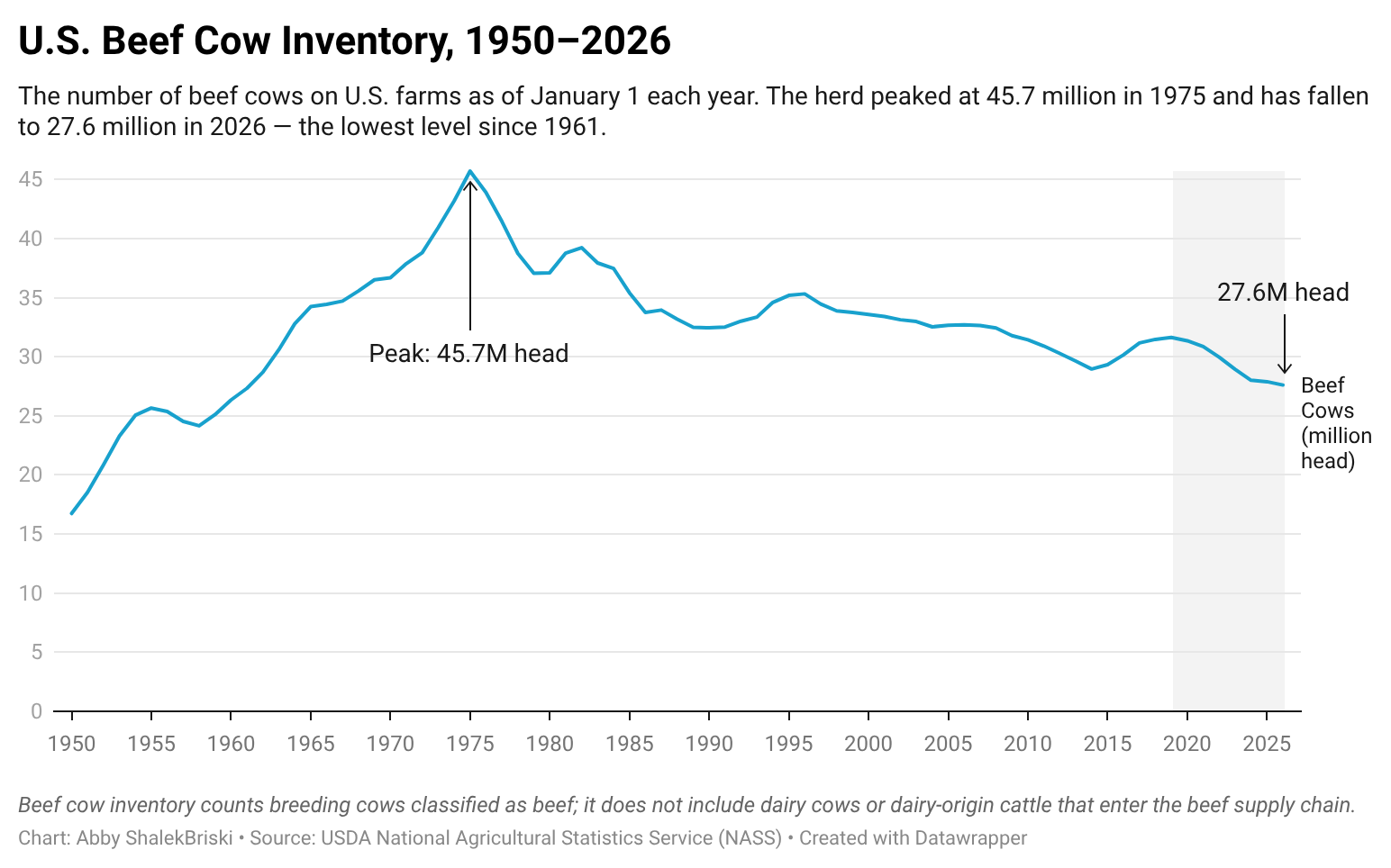

The U.S. beef herd, at approximately 27.6 million head of cows, is at its lowest level since the 1960s. The 2010s brought drought, low prices, and herd liquidation. While cattle prices have steadily increased since 2017, herd rebuilding remains slow, and beef prices remain high.

The reduction of the national herd and strong consumer demand for beef created an opportunity. Over the past decade, dairy farmers began to use artificial insemination (AI) to breed their cows with beef bulls (i.e., Angus, Limousin, etc). These beef-on-dairy cross calves are worth much more than a purebred dairy bull calf.

What started less than a decade ago as a sort of on-farm “side-hustle” has turned into a legitimate revenue stream and disrupted the way American beef operates. The adoption of beef-on-dairy has coincided with a steady upward rise in beef prices and a small national beef herd. Trade publications have framed these beef-on-dairy crosses as filling the gaps, providing a much-needed source of cattle for the market. Derrell Peel of Oklahoma State recently remarked that beef herds may start to slowly rebuild, however, due to the nature of herd building (cattle have ~9-month pregnancy plus take another 15 months of growing before that calf matures into a heifer mature enough to breed).

As the national beef herd thinks about rebuilding, the dairy industry isn’t waiting. Dairies have made structural changes to their operations, building a new revenue stream out of what was once a low-value calf. At what point does a dairy cow raising beef calves stop being a gap-filler and start being a competitor?

Keeping milk and meat separate

Dairy and beef have long acted as their own separate sectors with their own producer groups. They have a record of having separate lobbying priorities, trade associations, and even cultural identities.

They also run their businesses in radically different ways: Beef ranchers graze their cows on pastures or range. Cows are largely left to their own devices until it’s time for vaccinations, moving to a different pasture, or being shipped. Breeding is simple by design. Turn out a bull, let biology do the work, sort the calves at weaning. It’s a system built around land and low labor, and it has run the same way for generations1.

Dairies are a more intensive affair. Cows have to be milked multiple times daily and managed in controlled environments year-round. The majority of dairy cows are not simply let loose on large acreages to do as they like. Breeding is equally deliberate: meaning a straw of semen versus a bull in a pasture.

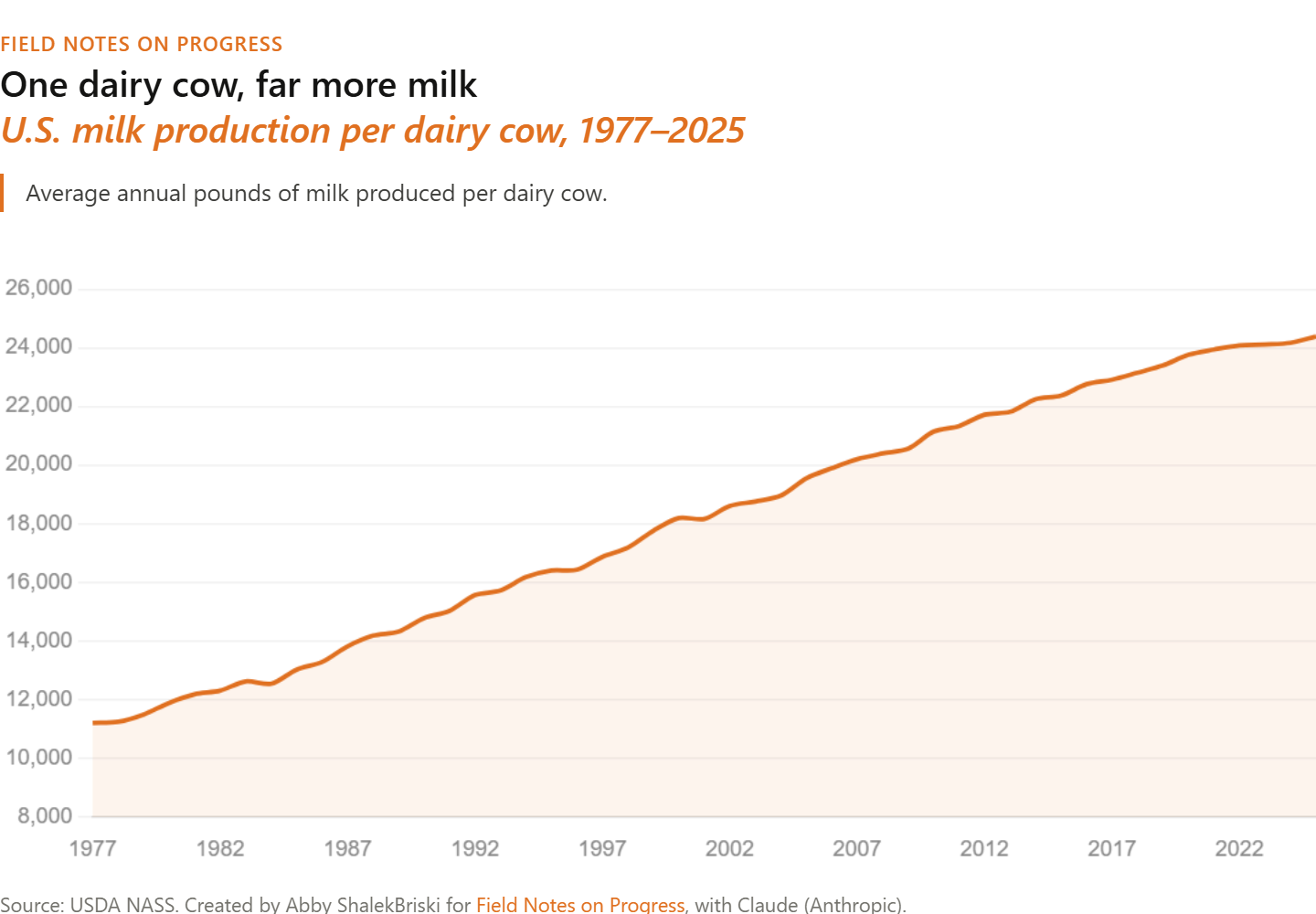

This bifurcation goes so deep that dairy and beef cows are essentially different animals. The average beef cow may produce 10-20 lbs of milk a day, while a modern Holstein dairy cow may produce 60-100+ lbs. Holsteins are bred to efficiently convert feed into milk, while a beef cow is more compact, heavily muscled, and bred to convert feed into muscle. They are optimized for entirely different means.

But as artificial insemination technology has grown more sophisticated, the dairy industry has slowly begun to build a presence in the beef industry. While it remains very difficult to produce a beef cow that makes as much milk as a Holstein, it is increasingly easier to produce a dairy cow that ends up as a Choice-grade steak.

Sexed semen and the accidental beef supplier

When farmers talk about AI disrupting industries, they don't mean chatbots. Artificial insemination (AI), the process of breeding a cow without a bull via a straw of semen, has been commercially practiced since the mid-20th century. Over the past several decades, AI technology has rapidly evolved. Genetic testing, improvements in collection and handling methods, and the ability to freeze and store semen have all reduced days between pregnancies, and pregnant cows generate revenue.

We primarily see AI used in the dairy industry, where cows walk through a milking parlor several times a day and are intensively managed, creating numerous opportunities to artificially inseminate them efficiently. This competitive dynamic can only run in one direction. A beef rancher cannot pivot to producing milk as an additional revenue stream. Beef cows aren’t as closely managed and simply cannot produce enough milk to justify the infrastructure that a dairy requires, such as a milking parlor. But a dairyman can simply pivot to beef with nothing more than a straw of semen. Once he knows he has enough replacement heifers for his milking operation, the dairyman can use his straw to fill every marginal cow uterus with a beef baby.

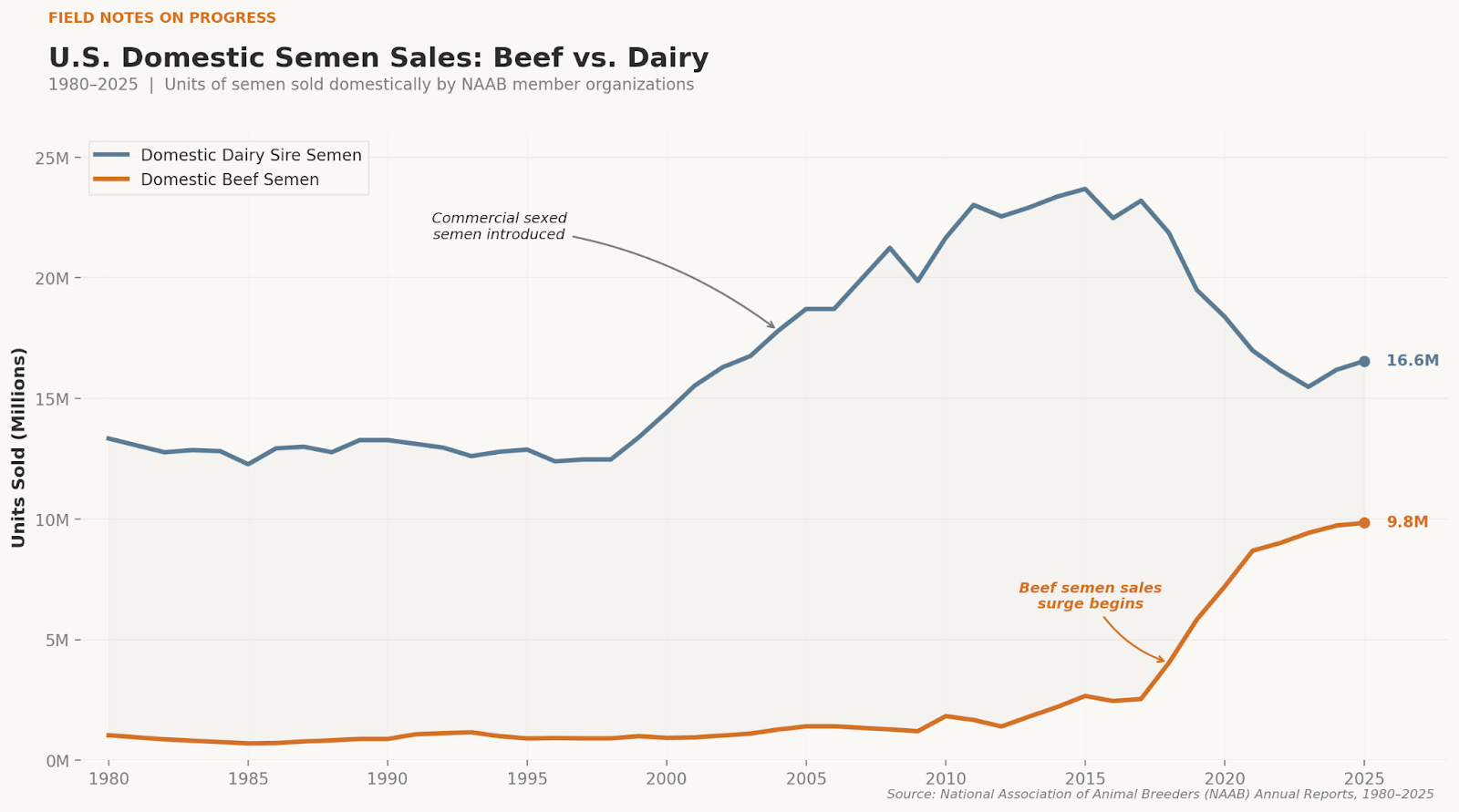

This is how sexed semen changed everything. For dairies, it is perhaps one of the most important innovations in reproductive technology. Dairy producers had the ability to choose the gender of calves. Gone was the coin flip of what you were going to get. All of a sudden, sourcing replacement heifers (heifers that come into your herd and replace cows that die or are culled) wasn’t so difficult. Previously, bull calves were usually sold shortly after birth for a low price. Their contribution to the whole farm revenue was marginal at best. With the introduction of sexed semen, a producer could control the percentage of heifer calves being born. There was a dairy heifer abundance!

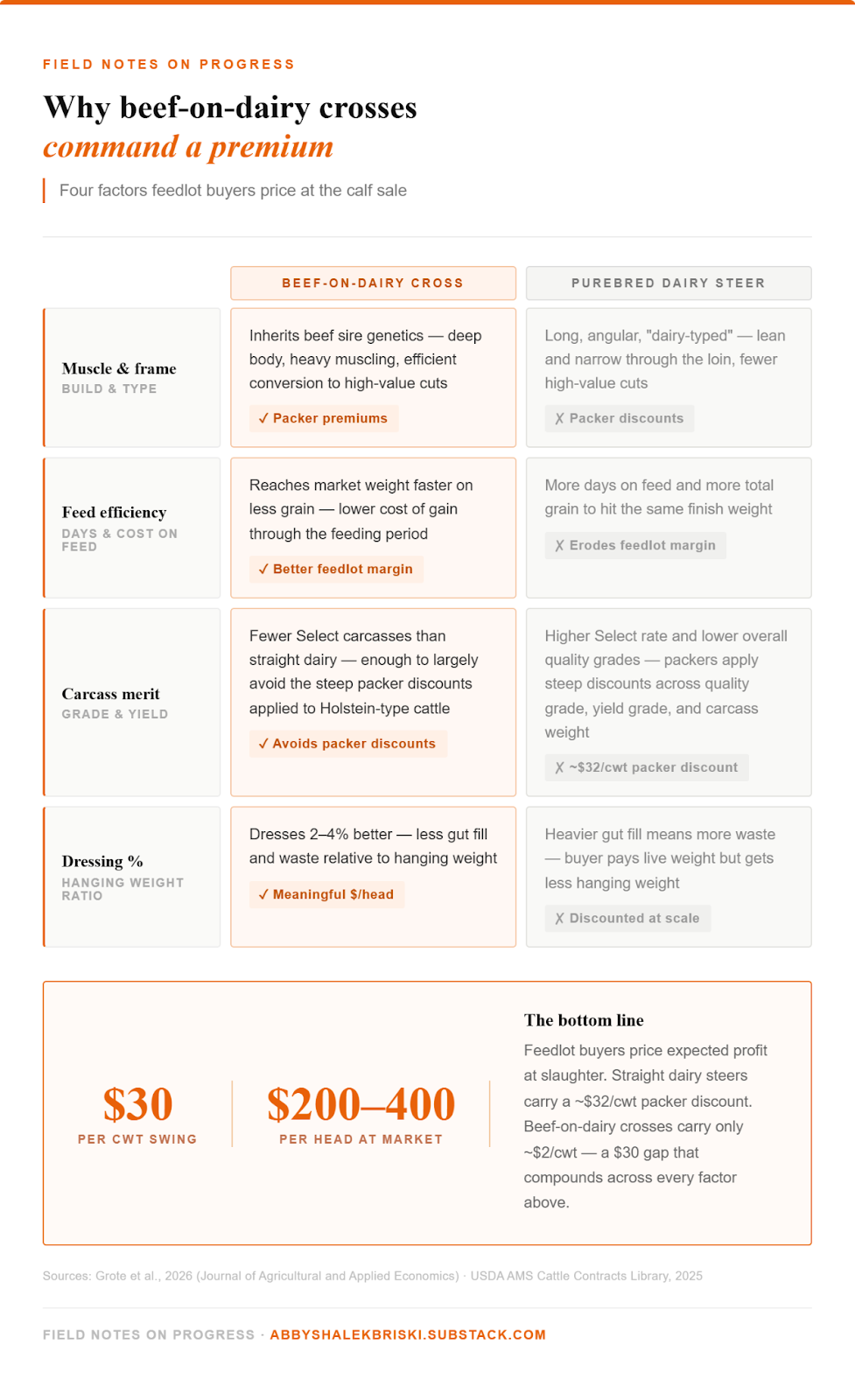

Accompanying this abundance was a realization: any breeding slot not needing to produce a replacement heifer could be used for something else. Herd managers started using beef semen. For example, a manager crossing a Holstein cow with an Angus bull gets a bull calf that splits the difference between the two breeds. The calf yields more muscling than a purebred dairy steer, might qualify for Certified Angus Beef premiums, and has better feed efficiency. Beef packers have discount straight-bred dairy steers, around $32 per cwt, because their carcasses are leaner, narrower, and yield less of the high-value cuts that come from a thick-loined beef animal. But beef-on-dairy crosses? Only about $2 per cwt. In a recent Oklahoma State feeding trial, beef-on-dairy crosses in calf-fed systems actually returned more per head than native beef calves raised in the same system2. These results will vary by region and genetics. Regardless, these preliminary results indicate the ability of beef-on-dairy crosses to compete economically with beef systems.

The beef begins

Dairy cattle going to beef is not new. Culls from dairy herds became ground beef or other low-value products. However, dairy has never meaningfully contributed to higher-end or more premium products, until the last decade.

For the past 50 years, dairies have pursued specialization, technology adoption, and intensive management. Traditionally, many agricultural operations had multiple enterprises (i.e., a varied crop mix, maybe crops and livestock, etc.). Part of this diversification strategy was risk management. If one enterprise had a poor year, perhaps whole farm profitability would be impacted less. Dairies moved in the opposite direction, betting on productivity per cow.

This singular focus, coupled with technology, has allowed huge gains in output and even reduced the use of inputs. It’s also left producers exposed when milk prices collapse. Now, through beef-on-dairy crossbreeding, dairies are diversifying again.

What most consumers think about is the steak in front of them. What the beef industry thinks about is breed, certification, and shelf placement. Certified Angus Beef (CAB) is the most widely recognized beef certification in the country. Its most famous requirement is that the animal must have a predominantly solid black hide. The real disqualifier is looking like a dairy cow: light muscling, wrong conformation. CAB keeps straight Holsteins out.

But cross a Holstein with an Angus bull, and the calf often comes out with a predominantly black hide and enough beef-type muscling to pass the live animal screen. Fed and finished correctly, industry experts estimate 25% to 45% of those crosses can qualify for the CAB label. Research confirms that consumers cannot distinguish them from conventional beef cattle on tenderness, flavor, or juiciness3. Beef-on-dairy crosses are not quietly entering the supply chain through ground beef and hot dogs. They are competing for premium shelf space at the meat counter, wearing the same label your butcher has been selling for decades.

This shift cannot be overstated. Between 2013 and 2024, beef semen sales in the United States increased 437%. Starting around 2017, the sale of purebred Holstein semen dropped.

Beef specialists estimate that in 2026, perhaps 15% of total cattle slaughter in the United States could be beef-on-dairy. This is double of what was estimated in 2022. Over the same period, the economics of dairies have changed. In January of 2026, revenue from beef calves and culled cows was more than double what many dairies were getting in 2022, while milk prices weakened sharply. For some producers, breeding dairy cattle with beef semen has become an important financial buffer.

Beef-on-dairy changed the terms of competition

For most of American agricultural history, the beef and dairy industries were organized around different economic problems. Beef producers generally favored open markets and limited government intervention. Dairy producers, facing chronic issues of perishability, surplus, and price volatility, have a long standing history of price supports and supply management. Specialization and genetic selection made different end products of their respective cows. Their policy agendas were distinct enough that direct conflict was relatively uncommon.

That separation is becoming harder to sustain.

In October 2025, the National Cattlemen’s Beef Association (NCBA) called on President Trump to keep beef imports from Argentina out of the domestic market. The objection itself was not surprising. Producers were feeling cautiously optimistic. Cattle prices were high. The national herd was small. And a growing share of the beef moving through American feedlots had never set foot on a ranch.

Two months later, the dairy industry made its own move. In January 2026, Western United Dairies, a California trade group, proposed a program called Make America More Ground Beef, or MAMGB, asking USDA to pay dairy farmers $1,800 to $2,000 per head to accelerate the culling of their herds. The stated goal was to add up to 1.1 billion pounds of lean trim to the ground beef supply and lower retail ground beef prices by 18 to 25 percent4. The American Farm Bureau Federation opposed the idea immediately. NCBA’s 2025 policy book explicitly rejects government intervention to set prices, underwrite inefficient production, or manipulate domestic supply, demand, cost, or price. USDA was later reported to have little interest in pursuing the proposal.

So the proposal was wildly unpopular with the associated industry. The interesting part is not the lobbying itself from the dairy industry. Agricultural groups lobby all the time. The interesting part was that both sides are now “beefing” over beef. Dairy producers were asking the government to help them move more product into it. Beef producers were trying to keep other sources of supply out of it. Perhaps beef-on-dairy has done more than raise the value of dairy calves. It had turned dairy and beef into direct political competitors.

The direct production effect of beef-on-dairy appears to be modest. A dairy cow was always going to produce a calf. Beef-on-dairy has the capacity to change the composition of cattle going to market more than the total number of cows. It raises the value of the calf out of a dairy cow more than it expands the number of cattle.

Someone from a beef background often thinks of cattle in a “value-added” framework. As cattle are raised, each step in the system captures value: weaning, vaccinating, backgrounding, finishing. Producers may earn additional premiums for raising cattle within certain standards, such as organic, pasture-finished, or a cooperative brand. Each producer understands what they’re working with, their land, their genetics, their buyer relationships, and tries to manage toward the best available market. The whole system is built around the idea that beef cattle, raised the right way through the right channels, are worth more than the sum of their inputs.

Dairy calves, historically, couldn’t access most of that system. A straight Holstein steer was discounted at the packer. It wasn’t competing for CAB premiums or natural program certifications. The channels were separate, and beef producers could build value in theirs without worrying much about the others.

That distinction has weakened. The same sexed semen technology that solved the dairy industry’s replacement-heifer problem also gave dairy producers a relatively low-cost way to redirect part of their breeding program toward beef production. From the standpoint of industrial organization, that is a meaningful change. It lowered the barrier to entry into higher-value beef channels for producers who were already operating at scale, already owned the facilities, and were already making breeding decisions. The beef rancher spent decades and significant capital positioning himself in that market. The dairy farmer got there with a straw of semen.

Thanks to Mike Riggs , Alexander Kustov , Rhishi Pethe , Jeff Fong , Deric Tilson, Garth Gatson , and Ryan Loy , all of whom read drafts of this piece at various stages and saved me from at least a few bad arguments, overclaims, and unfortunate phrasings. Any remaining errors, eccentricities, or excess enthusiasm about cattle reproduction are, of course, my own.

Due to land allocation and resource availability, there are a lot of creative ways to raise cows. This is a bit of an overgeneralization, but how the majority of producers do things.

Grote, A., DeVuyst, E. A., Radmehr, R., & Beck, P. (2026). Economic Analysis of Yearling-Fed and Calf-Fed Systems of Native Beef and Dairy-Beef Crossbred Steers. Journal of Agricultural and Applied Economics, 1-12.

Foraker, B. A., Frink, J. L., & Woerner, D. R. (2022). Invited review: a carcass and meat perspective of crossbred beef× dairy cattle. Translational Animal Science, 6(2).

I have not seen the actual modeling that allegedly happened. No one would ever produce it. I doubt this is what would have occurred if such a plan had come to fruition.

This is so fascinating!! I love that you covered so many aspects between beef and dairy, from cultural and technological differences, political aims, and diversification strategies

Very strong framing. The piece shows how technological control upstream can have consequences that look downstream like pricing conflict, lobbying conflict, and category confusion. A breeding tool did not just improve dairy economics; it altered the competitive geometry of the broader cattle industry. That is a much bigger story than “dairies found a better use for bull calves.”